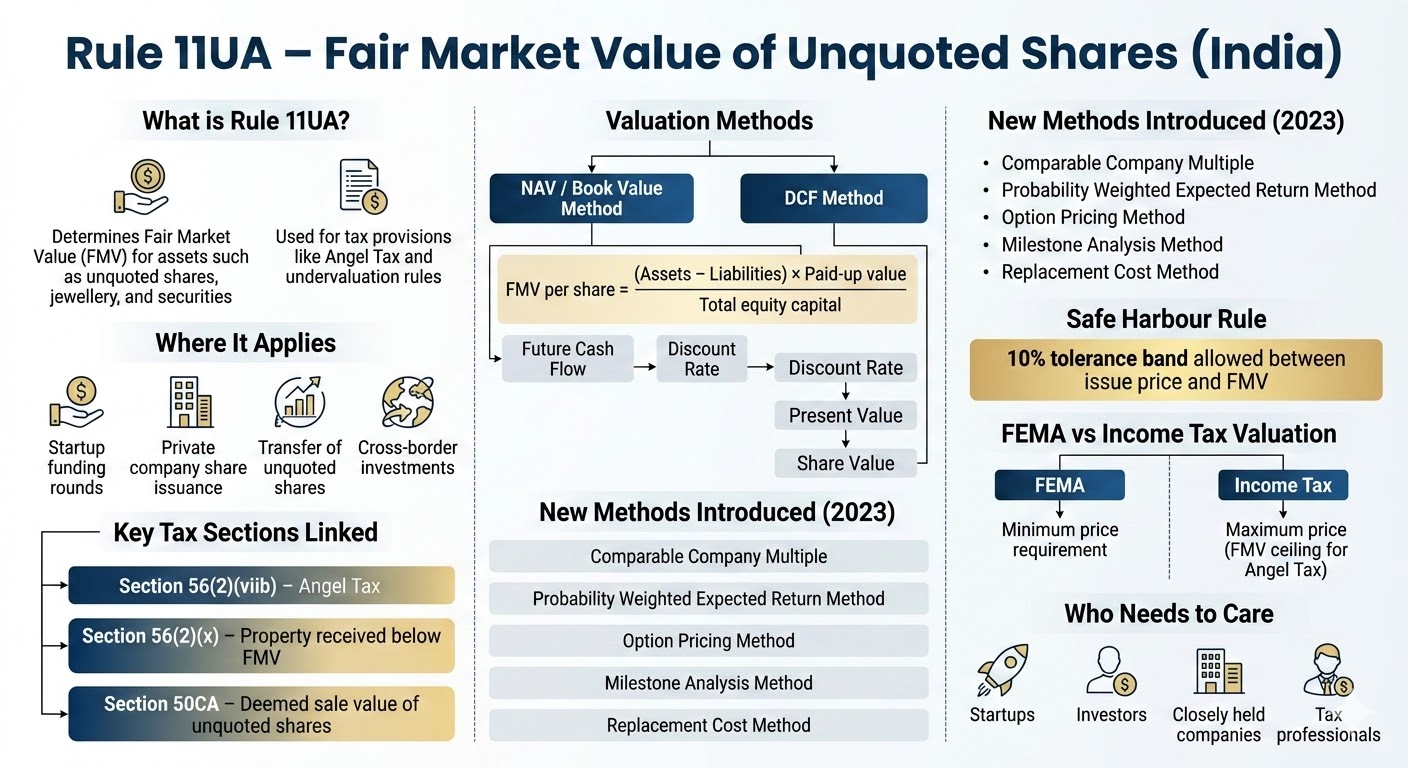

Rule 11UA of the Income-tax Rules, 1962 prescribes how to compute the Fair Market Value (FMV) of different types of assets, including unquoted equity shares and compulsorily convertible preference shares (CCPS).

This FMV is then used in various Income Tax provisions such as Section 56(2)(viib) (popularly called Angel Tax), Section 56(2)(x) and Section 50CA, especially where there is a suspicion of overvaluation or undervaluation of shares.

For startups, closely held companies and investors, understanding Rule 11UA is critical because it decides whether a premium on shares is tax-free capital or gets taxed as income.

Rule 11UA lays down standard formulas and methods to determine FMV of:

For unquoted equity shares, Rule 11UA(1)(c)(b) prescribes a specific book-value-based formula to arrive at FMV per share.

Separately, for Angel Tax under Section 56(2)(viib), Rule 11UA(2) allows valuation of unquoted equity shares by either the Net Asset Value (NAV) method or the Discounted Cash Flow (DCF) method, subject to conditions.

In essence, Rule 11UA answers a practical question: “What is fair market value in income tax for unquoted shares and certain other properties?”

The government introduced Rule 11UA to bring uniformity and reduce manipulation in valuation-driven tax provisions.

Without a standard rule, taxpayers and the department could endlessly dispute “value”, especially for private companies where there is no stock exchange price.

Key objectives include:

Rule 11UA is typically triggered for:

For Angel Tax under Section 56(2)(viib), Rule 11UA applies when a closely held company issues shares at a price higher than FMV; the excess is taxed as “Income from Other Sources” in the hands of the company.

For transfers of unquoted shares, Section 50CA may deem FMV (as per Rule 11UA) as the full value of consideration if the actual sale value is lower, resulting in higher capital gains for the seller.

For unquoted equity shares, Rule 11UA(1)(c)(b) uses a formula broadly based on:

FMV per share=A+B+C+D−LPE×PVFMV per share=PEA+B+C+D−L×PV

Where (simplified):

This formula is explicitly set out in Rule 11UA(1)(c)(b) and related guidance.

It is widely used when valuing unquoted equity shares for:

DCF values a company based on projected future cash flows discounted back to present value using an appropriate discount rate.

Rule 11UA(2) allows companies to choose DCF instead of NAV when issuing shares under Section 56(2)(viib), which is particularly relevant for startups and growth-stage companies whose value lies in future potential rather than current assets.

Historically, both Chartered Accountants and merchant bankers could certify DCF valuations under Rule 11UA(2)(b), but after Notification No. 23/2018 only SEBI-registered Category I merchant bankers are permitted to carry out DCF valuations for this purpose.

Rule 11UA(1) also covers valuation of:

These valuations are important for Section 56(2)(x), which taxes receipts of property without or for inadequate consideration.

To deal with cross-border investments and harmonise with FEMA/international practices, CBDT amended Rule 11UA in 2023 (Notification No. 81/2023, effective 25 September 2023).

For issue of shares to non-resident investors, five additional valuation methods were introduced alongside NAV and DCF:

These methods are widely used globally for startup and venture valuations and, for non-resident investments, must generally be applied by a Category I merchant banker. od (PWERM).

These methods must generally be applied and certified by a SEBI‑registered merchant banker, aligning Angel Tax valuation rules more closely with global and FEMA-style valuation practices.

Section 56(2)(viib) taxes a closely held company when it issues shares at a price that exceeds their FMV; the excess is treated as income from other sources in the hands of the company. FMV for this purpose is to be computed as per Rule 11UA – either by NAV/book value or by DCF / other notified methods, depending on who the investor is and which option the company chooses.

After 1 April 2023, Angel Tax provisions were expanded to include certain non‑resident investors as well, making the Rule 11UA valuation framework even more important for cross‑border startup funding rounds. However, DPIIT‑recognised eligible startups and specified investors such as venture capital funds, venture capital companies and notified funds continue to enjoy specific exemptions from Angel Tax within defined limits and conditions.

The 2023 amendments to Rule 11UA introduced a safe harbour of 10% in certain cases, meaning that if the issue price of shares is within 10% above the computed FMV, the variation may be ignored for purposes of section 56(2)(viib). This tolerance band recognises that valuation is not an exact science and reduces litigation over marginal differences between transaction price and theoretical FMV.

In practice, this allows some cushion when negotiating share prices, as long as the valuation is otherwise backed by a robust report and documentation.

Section 50CA deals with situations where unquoted shares are transferred at a consideration lower than their FMV; in such cases, the FMV as per Rule 11UA is deemed to be the full value of consideration for computing capital gains in the seller’s hands. Simultaneously, section 56(2)(x) can tax the buyer if the purchase price is below FMV, by treating the shortfall as income from other sources.

Thus, Rule 11UA and related rules (11U, 11UAA) effectively operate on both sides of the transaction – preventing the seller from understating consideration and the buyer from claiming an unjustified bargain, at least for tax purposes. Many professional articles highlight that valuation for 50CA and 56(2)(x) is generally based on the Rule 11UA(1)(c)(b) formula, and no separate merchant banker report is mandated for pure NAV-based calculations.

Across these provisions, “fair market value” under Indian income tax law is a defined, rule-driven figure – not an open-ended negotiation number. For specified assets, FMV is the value determined strictly in accordance with Rule 11UA (or related rules like 11U, 11UAA, 11UB, 11UC), using the prescribed formulae and methods.

This statutory FMV can differ from:

Because FEMA guidelines typically prescribe a minimum price for cross‑border share dealings, while income tax law (via section 56(2)(viib)) imposes a maximum price (ceiling) based on FMV, taxpayers often need to manage both simultaneously in foreign investment deals.

For any issue or transfer of shares involving non‑residents, FEMA (Foreign Exchange Management Act) regulations come into play, prescribing that shares cannot be issued or transferred below a fair valuation determined by an authorised valuer using internationally accepted pricing methods. This creates a dual compliance challenge: FEMA insists on a minimum price, while income tax law (via Rule 11UA and section 56(2)(viib)) taxes any price above the tax FMV.

Policy discussions and recent amendments explicitly aim to harmonise Rule 11UA with FEMA valuation norms, especially after Angel Tax was extended to foreign investors. In this context, a FEMA and tax expert can:

For startups and investors, working with a FEMA expert who also understands Rule 11UA is one of the most practical ways to de‑risk cross‑border funding and exit transactions.

Discussions on public forums such as Reddit and Quora often revolve around a few recurring practical doubts, which can be grouped as FAQs:

No. While Rule 11UA is heavily used in Angel Tax cases, it also applies whenever section 56 requires FMV of property other than immovable property, including for gifts of unquoted shares under section 56(2)(x) and for determining deemed consideration under section 50CA.

For pure NAV/book‑value calculations under Rule 11UA(1)(c)(b), there is no statutory requirement that a merchant banker or CA must certify the value, though many taxpayers obtain professional support for robustness. However, where the DCF method is chosen under Rule 11UA(2)(b) for section 56(2)(viib), the rules now require a SEBI‑registered merchant banker’s valuation report; chartered accountants cannot sign DCF reports for this specific purpose after the 2018 amendment.

Asset‑light, high‑growth startups usually prefer DCF, because the NAV formula can undervalue them when current assets are low but future potential is high. However, DCF brings subjectivity and greater scrutiny, especially after Angel Tax was tightened for foreign investors, so there is often a trade‑off between a more realistic valuation and litigation risk.

If unquoted shares are sold below FMV, section 50CA may deem the FMV as the sale consideration for capital gains computation, which is determined as per Rule 11UA. At the same time, if the buyer acquires shares cheaper than FMV, section 56(2)(x) can tax the buyer on the discount, again using the Rule 11UA FMV, so both sides must consider the valuation impact before structuring transfers.

Post‑2023 changes, Angel Tax under section 56(2)(viib) has been extended in principle to many non‑resident investors, but exemptions continue for DPIIT‑recognised startups and specified investor classes such as venture capital funds, venture capital companies and notified entities. Foreign investors therefore need to check both: whether the company is an eligible startup and whether they fall into a notified safe category before assuming Angel Tax is not a concern.