Form ODI is the main RBI reporting form for Overseas Direct Investment (ODI) by Indian residents in foreign joint ventures and subsidiaries. It captures who is investing, where, how much, and how the overseas entity is performing over time.

Overseas Direct Investment (ODI) means a direct investment made by a person resident in India into a foreign entity by way of equity capital, compulsorily convertible instruments, or other eligible financial commitments, usually in a joint venture (JV) or wholly owned subsidiary (WOS). The foreign entity must be engaged in a bona fide business activity, and the investment is regulated under FEMA (Overseas Investment) Rules, 2022 and related Regulations and Directions.

ODI is outward investment from India into a foreign company, while Foreign Direct Investment (FDI) is inward investment from non‑residents into Indian companies. In ODI, an Indian entity or resident individual becomes shareholder or owner abroad; in FDI, a foreign investor takes a stake in an Indian business.

ODI today is governed mainly by:

RBI also issues A.P. (DIR Series) circulars that give practical instructions on forms, online reporting, late submission fee, and sector‑specific conditions.

ODI helps Indian businesses expand markets, access technology, raw materials, and brands abroad. It can also improve global branding, diversify risk across countries, and increase India’s export potential through overseas platforms.

The Reserve Bank of India (RBI) is the main regulator for ODI under FEMA. RBI sets eligibility rules, financial limits, reporting formats like Form ODI / Form FC, and monitors transactions through authorised dealer (AD) banks.

Under the Overseas Investment Rules, “person resident in India” can make ODI if conditions are met. Eligible investors include:

Entities classified as wilful defaulters, NPAs, or under investigation need additional clearances or may be restricted.

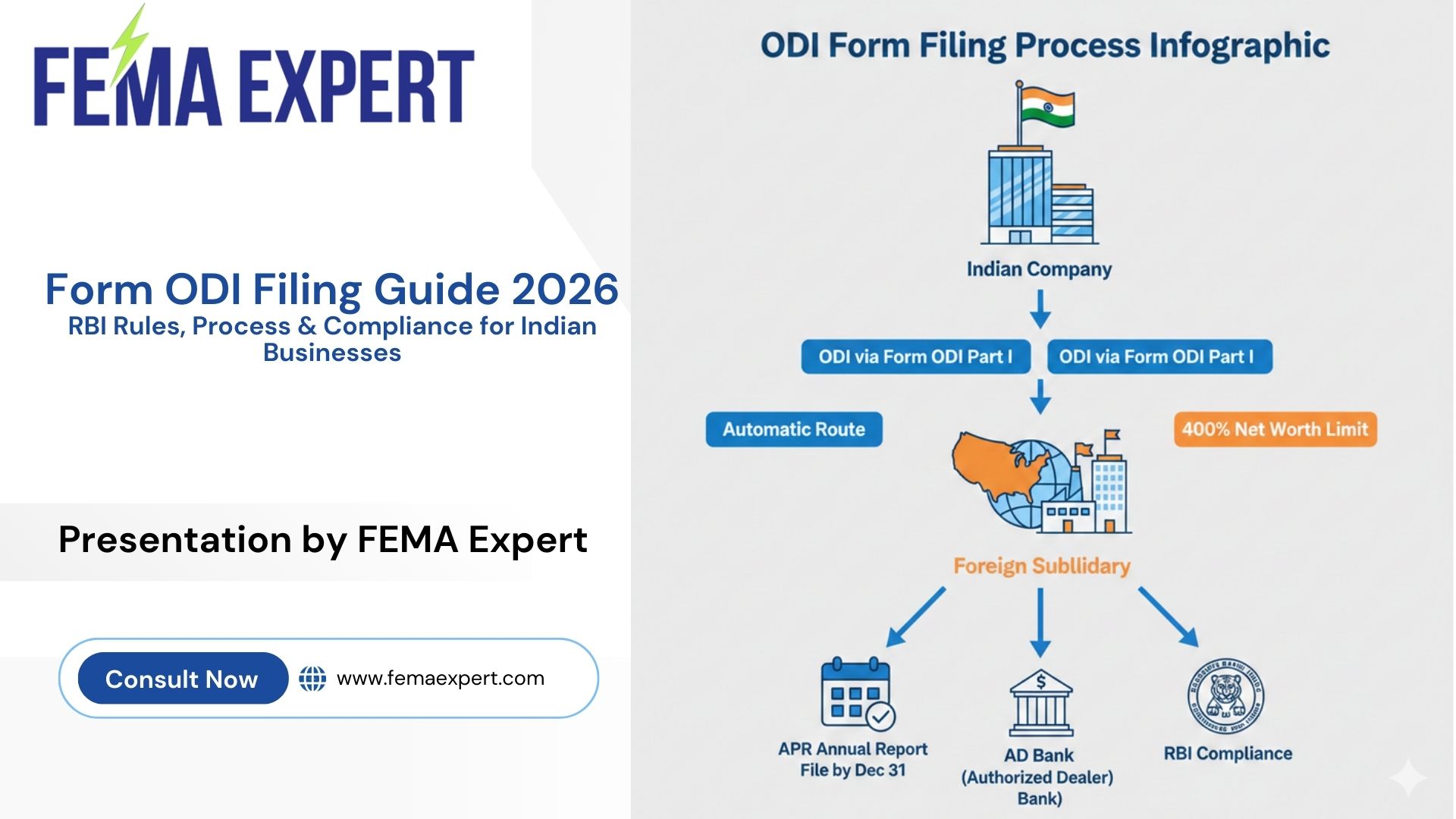

Most ODI is now permitted under the Automatic Route if it satisfies all conditions like sector eligibility, financial commitment limits, and clean compliance history. No prior RBI approval is needed in this route, but you must follow strict post‑investment reporting and limits such as overall financial commitment up to 400% of net worth.

If the proposal does not meet automatic route conditions (for example, in restricted sectors, complex structures, or where limits are breached), prior RBI approval under the Approval Route is required. These cases undergo detailed scrutiny of business rationale, structure, and risk, and timelines are longer.

Key compliance under the ODI framework includes:

Non‑compliance can lead to late submission fee (LSF), restriction on further ODI, and FEMA penalties.

Form ODI is the RBI reporting form for Indian parties and resident individuals making ODI in a foreign JV/WOS. It captures details of the Indian investor, foreign entity, type and amount of financial commitment, remittances, performance, and disinvestment.

Traditionally, Form ODI has four parts:

In practice, online ODI modules may combine some parts, but the same information blocks are still required.

Form ODI is required when a resident Indian entity or individual:

Filing is routed through the designated AD Category‑I bank, which in turn reports to RBI.

A simple workflow is:

For complex cases, work closely with a FEMA Expert so that structure and documentation are correct from day one.

Typical documents include:

Your AD bank may ask for extra papers depending on risk and sector.

Key timelines under the current regime are:

Delays attract late submission fee, and continuous default can lead to FEMA compounding and restrictions.

Some frequent pitfalls are:

A FEMA Expert or specialised ODI consultant can help you avoid these issues.

To set up a foreign subsidiary (WOS):

The designated AD Category‑I bank is your first regulator in practice. It verifies KYC, checks eligibility and limits, files forms in RBI’s system, allots or obtains UIN, and monitors ongoing compliance like APR and disinvestment reporting.

Once ODI is made, you must file Annual Performance Report (APR) each year through the AD bank for every foreign JV/WOS. APR reports key financial data like turnover, profit or loss, net worth, outstanding dues, and any further investments or guarantees.

APR must be filed by 31 December for the previous financial year, even if the foreign entity has no operations or profit.

When you sell shares, liquidate the foreign entity, or write off investment, you must:

Improper or unreported disinvestment can invite FEMA non‑compliance.

ODI has tax angles both in India and in the host country.

You should always pair FEMA planning with income‑tax and DTAA advice.

When an Indian investor transfers or disinvests shares of a foreign JV/WOS, capital gains must be computed as per Indian tax law, considering cost and holding period. The transaction must also be reported to RBI, and proceeds repatriated as per FEMA rules.

If you delay or miss ODI or APR reporting:

Serious or wilful violations may face compounding or penalties up to thrice the amount involved under section 13 of FEMA.

The big change is the New Overseas Investment framework notified in August 2022, which replaced older ODI regulations and clarified concepts like ODI vs OPI, financial services investment, and round‑tripping. RBI has also standardised Late Submission Fee across FEMA reporting and moved most filings to online portals, making AD banks the main gatekeepers.

Because rules and portals keep evolving, always check the latest RBI circulars or consult a FEMA Expert before large or complex ODI.

Startups and SMEs use ODI to acquire small foreign brands, open sales offices, or set up holding companies in strategic jurisdictions. However, they must be extra careful about:

Here, ongoing support from a FEMA Expert and tax advisor can save time and future penalties.

Imagine an Indian SaaS company in Bengaluru that wants to sell to US clients and decides to set up a wholly owned subsidiary in Delaware.

1. Is ODI allowed under automatic route for most sectors?

Yes, most bona fide business activities are permitted under automatic route, subject to sectoral restrictions and overall limits; otherwise, RBI approval is required.

2. What is the current financial commitment limit for ODI?

An Indian entity’s total financial commitment (equity, loans, guarantees, etc.) in all foreign entities normally cannot exceed 400% of its net worth under the automatic route.

3. Is APR required even if the foreign company has no turnover?

Yes, APR is mandatory every year for all ODI‑linked foreign entities, even if there is no income or operations.

4. Who actually submits Form ODI to RBI?

The designated AD Category‑I bank uploads Form ODI / relevant sections in RBI’s online system based on information and documents given by the Indian investor.

5. What is the due date for APR?

APR in respect of ODI must generally be submitted by 31 December for the previous financial year.

6. How is late submission fee for APR calculated?

For APR / Form ODI Part II and some similar returns, RBI has prescribed a flat LSF of ₹7,500 per delayed return.

7. Can individuals make ODI?

Yes, resident individuals can make ODI in permitted manners, usually under Liberalised Remittance Scheme, with specific caps and additional conditions.

8. Is investing back into India through multiple layers allowed?

The new framework restricts “ODI‑FDI structures” with more than two layers of subsidiaries to curb round‑tripping.

9. Should I always involve a FEMA Expert?

For any meaningful ODI, especially where tax, valuation, or complex structures are involved, working with a FEMA Expert and cross‑border tax advisor is strongly recommended to stay compliant and penalty‑free.